The development of Australia’s innovation capability is connected to the pressing need for environmental sustainability due to global warming, and rising security concerns stemming from reliance on supply chains dominated by China, and related vulnerabilities of trading partners.

These arise in the context of escalating geopolitical tensions, particularly between the United States and China vying for technological supremacy. To address these simultaneous challenges, Australia needs a proactive policy framework to enhance its innovation capability as a form of insurance policy preparing for an uncertain future.

This framework should underscore the multi-dimensional aspect of innovation, foster essential collaboration between diverse stakeholders within innovation ecosystems, and align national interests with long-term sustainability goals.

A nation’s innovation capability is its consolidated capacity to generate, disseminate, and commercialise new ideas, technologies, products, services, and processes. As a multifaceted activity engaging a variety of stakeholders, innovation has evolved into a complex, iterative endeavour requiring concerted efforts from a diverse array of actors in innovation ecosystems.

These actors include governments, universities and research institutes, large corporations, small and medium-sized enterprises (SMEs), entrepreneurs, investors, non-governmental organizations (NGOs), and philanthropic organisations.

Because of this complexity, consideration of Australia’s innovation capability must extend beyond questions of its efficiency, in terms of turning inputs into innovation into outputs, to issues of its effectiveness, especially how it integrates into international supply and production chains and deals with sustainability challenges.

This article argues how Australia’s national innovation capability depends on the performance of Australian firms in the context of an increasingly narrow and precarious trade and industrial structure, and systemic productivity slowdown and associated wage stagnation.

Using the example of clean energy transition, it contends that government policy must address how actors in Australia’s innovation ecosystems engage nationally and globally in the face of massive political and technological uncertainty.

Innovation efficiency and effectiveness

Traditional measures of innovation capability tend to treat innovation as a linear series of activities, gauging performance using a single ratio of innovation outputs to inputs, such as patents to R&D expenditure.

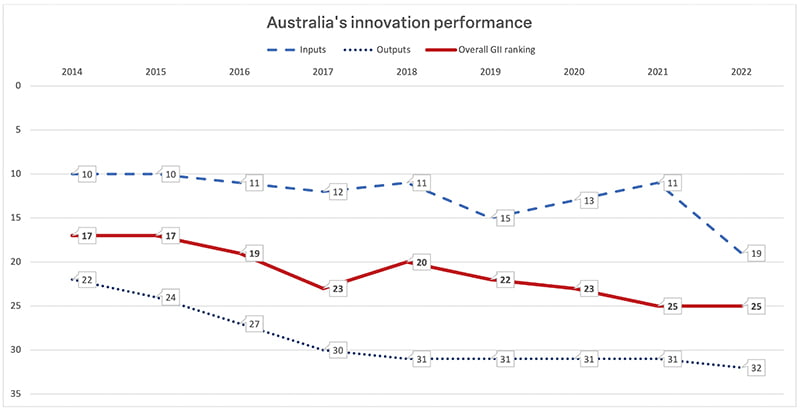

According to the 2022 Global Innovation Index (GII), Australia ranked 19 in innovation inputs, but only 32 in innovation outputs, leading to an overall rank of 25. Despite strong performance in measures of innovation inputs (except in 2022), Australia’s overall innovation performance has declined, slipping from 17th place in 2014 (see Figure 1).

The primary factor contributing to this drop is a decrease in measures of its innovation outputs. Australia’s overall strengths in innovation lie in its substantial investments in supportive human capital, institutions, and infrastructure, its performance in producing innovation outputs, including patents, high-tech manufacturing and exports, intangible assets, including intellectual property, global brand value, as well as production and export complexity, has been relatively weak.

This position in innovation is notably lower than its 13th place in economic development as measured by GDP. From this perspective, these metrics suggest a disconnect in Australia’s ability to transform innovation investments into tangible outputs, indicating a deficiency in innovation capability.

Such measures, however, only provide an incomplete and piecemeal picture of innovation capability and performance. They fail to capture the intricate interdependence and the distinct stages between knowledge creation and commercialisation, as outlined in the innovation value chain of complex technologies in modern society.

They also fail to ascertain numerous important contributors to innovation capability, such as firm and industry responsiveness, agility, and resilience, and ability to contribute to environmental sustainability.

Furthermore, the increase in value added intangible assets has become more pronounced over the past two decades, driven by the specialisation of innovation capabilities and increasing technological complexity of modern products and production processes.

As a result of these factors, the efficiency of innovation in terms of inputs and outputs can no longer fully capture the effectiveness of converting knowledge into value. This conversion process often involves multiple inputs and outputs from different organisations across the global value chain.

Innovation effectiveness may be seen as the extent to which an innovation accomplishes its intended outcomes and contributes to an economy or organization’s overarching objectives.

This involves evaluating the impact of various facets of innovation, such as R&D, product design, organisational and operational processes, marketing strategies, and linkage structures in a value chain.

Innovation capability in firms

Australia’s innovation performance reflects its economic structure, and particularly the crucial activity of firms, whose ‘dynamic capabilities’ allocate and reconfigure resources for innovation.

As Sutton (2012) argues, “…the proximate cause [of differences in wealth among nations] lies, for the most part, in the capabilities of firms.”

Of the top ten Australian companies (with headquarters in Australia) featured among the world’s 500 companies by market value (as of December 2022), only two – CSL and Atlassian, ranking 3rd and 10th respectively – are technology companies, alongside resources and financial services firms.

Unlike other small yet innovative nations, such as Switzerland, Sweden, and South Korea, Australia lacks multinationals or globally recognised brands in key technological areas, which profoundly influences their innovation capability.

The R&D intensity of leading Australian firms is marginal compared to global technology giants which not only invest heavily in R&D but also act as ‘hubs’ in their respective innovation ecosystems, promoting co-investment and the co-creation of value with many international collaborators and complementors.

SMEs and micro firms play a significant role in Australia’s industrial structure. They employ 99.8 per cent of the workforce, with small enterprises (fewer than 20 employees) making up 97.5 per cent and medium businesses (20-200 employees) the remaining 2.3 per cent.

These SMEs, specifically those with an annual turnover of $10 million or less, constitute 98 per cent of Australian businesses. Small size limits the scale and ambition of innovation investments typically achieved by larger corporations.

Australia does, however, have some strong technology companies. Even though Australia ranks 37th globally for its ‘entrepreneurship policies and culture’, the country boasts nine unicorns (startup ventures with a market valuation of one billion or above), surpassing its proportional share of global GDP.

All Australian unicorns are in the high-tech sector, with several of these ventures becoming category-leading global businesses. Their global scale-ups leverage the power of networks, meaning that their commercialisation successes are based on innovation through light asset, digital platforms, not embedded manufacturing capabilities.

The shortcomings on innovation capability in Australian firms are not all related to industrial structure, with persistently identified shortcomings in managerial and innovation skills.

This is compounded by fragmentation and incoherence in the national policy framework, with generally sub-scale research and innovation programs spread haphazardly across 13 government departments and 150 separate budget line items at the Commonwealth level, not to mention duplication and misalignment with State programs.

Innovation capability in manufacturing

Manufacturing industry, as a locus of R&D, source of investment in skills and training, and producer of exports, is a crucial component of innovation capability. Australia’s R&D investment as a whole has seen a decline in recent decades.

R&D intensity, calculated as the ratio of a country’s R&D expenditure to GDP, fell from 2.4 per cent in 2014 to 1.8 per cent in 2021 – below the OECD average of 2.7 per cent.

Australia’s figure is significantly lower than that of the world’s leading industrial countries such as Germany, Japan, and the United States, all of which spend more than 3 per cent of their GDP on R&D.

It is also lower than innovation-driven countries such as South Korea and Israel, which invest more than 5 per cent of their GDP in R&D. China, an emerging innovator, recorded R&D spending at 2.55 per cent of its GDP in 2022.

Both Coalition and Labor governments claim plans to increase the nation’s R&D investment, aiming to reach the ‘magic mark’ of 3 per cent of GDP. It remains unclear, however, what is the mechanism by which this objective will be achieved, or where these funds are to be directed to most effectively enhance Australia’s innovation capability.

The urgency of this task is now becoming apparent, particularly as the funding of research is increasingly reliant on universities’ international student fee income. And much of this is absorbed by health and medical research.

Australia’s relatively low investment in R&D can be attributed to its reduced capabilities in manufacturing. In addition to its comparatively low R&D expenditure, Australia is also ranked as one of the least economically complex countries, as measured by the diversity and research intensity of its export mix, currently standing 91 globally.

Blessed with an abundance of natural resources, mining exports contribute nearly 14 per cent to the country’s GDP, with over 30 per cent of these exports shipped to China in 2022.

While Australia has avoided the traditional ‘resource curse,’ it’s resource booms over the past thirty years have led to cyclical volatility, including appreciation of the dollar, which in turn has diminished the competitiveness of other exports, particularly in manufacturing.

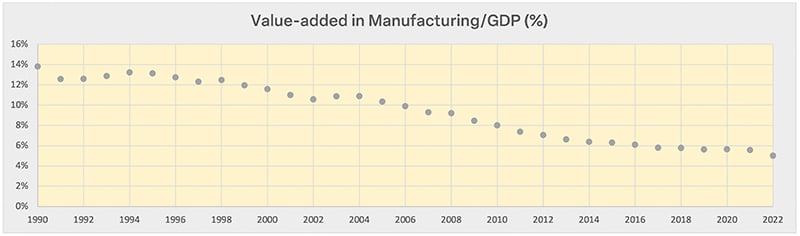

Value-added in manufacturing as a percentage of GDP has declined from almost 14 per cent in 1990 to 5 per cent in 2022 (See Figure 2).

Australia is not alone in experiencing the erosion of manufacturing capabilities. The shift to off-shoring and advances in innovation at the end of the 20th century saw more resources being directed in the West into R&D, design, intellectual property, branding, and marketing, while lower-value-added manufacturing jobs were outsourced to less developed nations, predominantly China, providing a ticket for China’s entry to global production networks.

At the same time Industry 4.0 smart manufacturing has become a key component of innovation. As an example, improvements in solar technology over the last decade have been driven less by scientific breakthroughs – a domain in which Australia has made significant contributions – and more by cost reductions through efficient production, a process in which China dominates 90 per cent of the value chain.

China’s burgeoning innovation prowess is significantly rooted in its manufacturing ecosystem and its technological advances have emerged not solely from universities and research labs, but largely from the learning and experimental processes generated by mass production.

The country has implemented a strategy of promoting manufacturing and secured unmatched cost advantages and considerable technological progress on a global scale through mass production.

Aware of its dependence on China’s manufacturing might and the importance of manufacturing economically and socially, and in an effort to regain its edge in emerging technologies, the United States has begun to revive its own manufacturing capabilities through strategies such as re-shoring, near-shoring, and friend-shoring.

This revival has proven to be a formidable task, as demonstrated by Apple’s experience in onshoring manufacturing capabilities for desktop computers in Texas, and TSMC’s efforts to construct a foundry for advanced chipmaking in Arizona, where obstacles included a shortage of skilled labour that is also expensive, and most importantly, the complexities involved in scaling production outside of established industrial ecosystems.

Innovation capability and clean energy transition

For decades, Australia has been a substantial exporter of energy commodities, mainly to China, contributing significantly to the country’s robust economic performance and its carbon emissions.

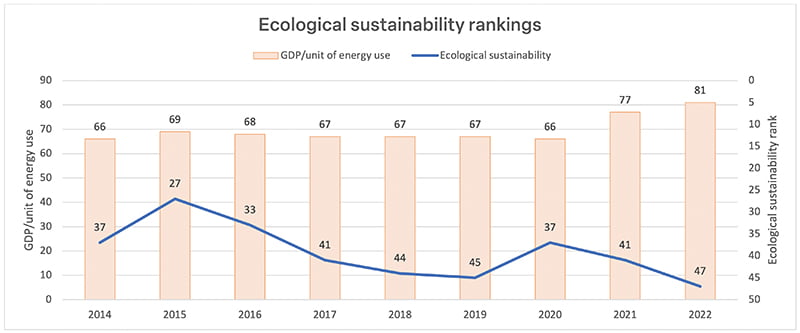

As depicted in Figure 3, Australia’s global rankings in sustainability – measured by overall geological sustainability and GDP per unit of energy use – have been on a downward trend over the past decade.

How the nation transitions to clean energy is crucially connected to its innovation capability and its ability to respond to global political tensions and decarbonisation opportunities.

Australia’s response to climate change has to be seen in the context of global policies, such as the US Clean Energy for America Act, which is seeing massive levels of investment around the world in clean technologies.

Given Australia’s natural endowments in critical minerals crucial for a clean energy transition, the country holds a pivotal role in the US-led ‘Minerals Security Partnership.’ This initiative aims at fostering a supply chain independent of China’s influence. In alignment with the US initiative, Australia plans to allocate $3 billion from its $15 billion National Reconstruction Fund towards renewable energy and low emissions technologies.

This proposal underscores Australia’s commitment to domestically produce clean energy components and process key minerals, such as lithium. While Australia produces 50 per cent of the world’s lithium, it captures only 0.53 per cent of its final value.

Despite advanced technological capabilities in resource extraction, there are, however, substantial obstacles to scaling production and advancing up the global value chain, due to the absence of a robust domestic manufacturing ecosystem and supportive infrastructures, heightening Australia’s supply chain vulnerability.

It is also imperative to take lifetime carbon emissions into account. While clean energy technologies such as solar panels, wind turbines, and electric vehicles are carbon-neutral during use, their production processes can carry significant environmental impacts. For instance, lithium extraction and processing are energy-intensive activities that contribute to carbon emissions.

A recent opinion piece in Nature underscores the importance of considering the entire lifecycle of clean energy technologies to effectively mitigate their carbon footprints.

The establishment of onshore lithium processing facilities in Australia would entail a significant investment in technology and expertise for processing and waste management, let alone investment in infrastructure such as electricity.

The transition to clean energy, therefore, emphasises the systemic nature of innovation capabilities within innovation ecosystems.

Associate Professor Dr Marina Yue Zhang is an Associate Professor at the UTS Australia-China Relations Institute. Prior to this position, Marina worked for UNSW in Australia and Tsinghua University in China. Marina holds a bachelor’s degree in biological science from Peking University, and both an MBA and a PhD from ANU. Her research interests cover innovation policy and practice, focusing on industries such as semiconductors, clean energy transition, cyber security and biopharmaceuticals. She is the author of three books, including “Demystifying China’s Innovation Machine: Chaotic Order” (OUP, 2022). Marina writes extensively on the intersection of technology and international relations.

Professor Roy Green is Emeritus Professor and Special Innovation Advisor at the University of Technology Sydney, where he was Dean of the UTS Business School. He has published widely in the areas of industry and innovation policy, including projects with the OECD and European Commission, and led a number of government inquiries. Currently Roy chairs the Advanced Robotics for Manufacturing (ARM) Hub, Food Innovation & Agribusiness Ltd (FIAL) Industry Growth Centre and the

Port of Newcastle, and he is a board director of the SmartSat CRC and a member of the Australian Design Council and NSW Modern Manufacturing Taskforce.

Professor Mark Dodgson, AO is currently Emeritus Professor at the University of Queensland; Executive-in-Residence at the University of Oxford; and Visiting Professor at Imperial College London. He has published 19 books and over 100 academic articles on innovation and entrepreneurship, and has researched and taught the subject in over sixty countries. Mark has advised numerous companies and governments throughout Europe, Asia, and North and South America and has been on the Boards and Advisory Boards of two multibillion-dollar companies and five start-ups. His current research is on the Oxford/AstraZeneca Covid-19 vaccine and the development of fusion energy.

Purchase a copy of the The Capability Papers here.

Do you know more? Contact James Riley via Email.