The world will decarbonise, fast or slow, hell or high water.

The hard part of the transition is more difficult than any deliberate undertaking ever previously contemplated. The very hard part is diabolically difficult. The hard part is the elimination of fossil fuels, collectively responsible for nearly three quarters of global emissions. The very hard part is eliminating emissions from agriculture, industry, land use change, and waste decomposition.

Let’s focus on the hard part. We need to transition from the Industrial Age ushered in by fossil fuels to the Electric Age ushered in by zero-emissions electricity. Electricity is like magic, and it can be used to replace most uses of fossil fuels.

Where the electrons are directly applicable, we should use them straight from their source. Such applications include battery charging for electric vehicles, heat pumps for homes, steam generation in factories.

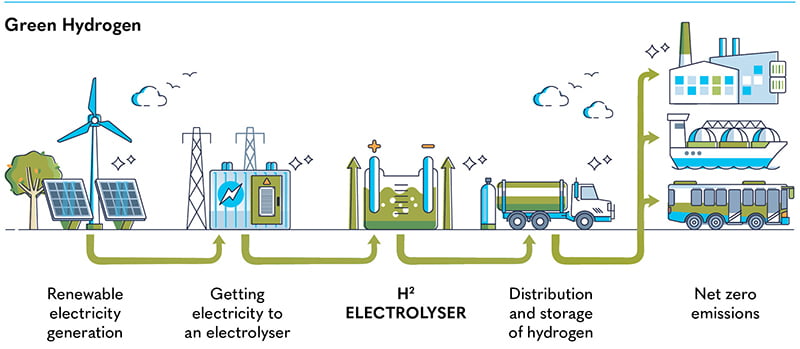

Where the electrons are not directly applicable, we can use chemicals that are themselves produced by zero emissions electricity. Many of the important chemicals are combinations of hydrogen, carbon, oxygen, and nitrogen. Hydrogen can be made by using electricity to split water into its constituent parts.

Carbon, in the form of carbon dioxide, can be captured from the atmosphere using electricity to drive fans and capture and release cycles. Nitrogen and oxygen can be plucked from the atmosphere using electricity for cooling and liquid fractionation.

Using yet more renewable electricity, these ingredients can be synthesised to produce decarbonised versions of existing products, such as ammonia, fertiliser, methane, methanol, ethanol, and kerosene.

Importantly, the markets for the fossil-fuel derived and produced versions of these chemicals already exist. And they are huge. For example, kerosene is the saturated hydrocarbon also commonly known as jet fuel – the irreplaceable liquid fuel that powers mid-size and large aeroplanes and helicopters.

End users driven by government policies and their own understanding of climate science want to purchase decarbonised versions of these important products, but despite being well motivated they are not prepared to pay more than a small premium over the existing high-emissions versions.

Taking the green premium out of the decarbonised products needs funding, early adopters, policy support, and innovation. International funding for clean technology already exceeds US$1 trillion per year and more is lined up in pursuit of future profits. There are many early adopters at all levels of consumption willing to pay a bit more to help the industries grow.

There are historical examples of successful government policy support, such as the solar subsidies in Germany, mandates in China, and the Renewable Energy Target in Australia. More recent policy initiatives include the Inflation Reduction Act introduced in the United States last year and the Rewiring the Nation fund budgeted this year in Australia.

Nevertheless, ongoing policy development will be necessary for this difficult transition. So, too, will ongoing innovation be necessary, because unlike solar, wind, batteries, and electric vehicles, very little in the technologies for producing decarbonised products is mature or operating at scale. Let’s look at three of them, starting with ammonia.

Globally, large quantities of ammonia are used to produce the nitrogenous fertilisers that are a significant enabler of agricultural productivity. The dominant means of producing ammonia is fossil-fuel based.

Natural gas (methane) is converted to hydrogen in steam methane reformers that produce large amounts of carbon dioxide from the chemical reaction and additional carbon dioxide from burning natural gas as a fuel to provide process heat and pressure.

Separately, more natural gas is burned to provide electricity to extract nitrogen from the atmosphere. Even more natural gas is consumed to run the venerable Haber Bosch process that combines the nitrogen and hydrogen into ammonia.

Finally, even more natural gas is used to power the production of urea that is the main ingredient of nitrogenous fertiliser. The main message from this list is that making green fertiliser is not simply a matter of making green hydrogen.

That is hard enough, but on top of that there is work to be done to develop processes and equipment that entirely replace natural gas with electricity to fuel nitrogen extraction, ammonia synthesis, urea synthesis and fertiliser production. Put out the call – innovation required!

Next, let’s look at jet fuel. While batteries will be used in short-haul aeroplanes with small numbers of passengers, and hydrogen might be used in medium-haul aeroplanes with modest numbers of passengers, there is no realistic alternative to jet fuel for long-haul aeroplanes with large numbers of passengers. It is inconceivable, based on what we know today, that any of us will board a battery-powered aeroplane in Sydney with 350 fellow passengers to fly non-stop to Dubai.

Long-haul flights are possible because of the almost ideal characteristics of jet fuel. It has high energy density, it does not freeze when cruising in the stratosphere at 60°C below zero, and it does not boil when the plane is taxiing on the runway in Dubai on a 50°C hot day. Unfortunately, when fossil-derived jet fuel burns, large quantities of carbon dioxide are emitted.

There are two ways to produce low-emission, drop-in replacements for existing jet fuel. One is to start with biomass. The most efficient process to produce jet fuel from biomass needs hydrogen and a substantial number of refining and synthesising steps. The other way relies entirely on electricity to absorb carbon dioxide from the atmosphere, produce hydrogen from water, then combine them in a synthesis pathway to produce kerosene.

While much work has already been undertaken, there is still much to be done to ensure that all the steps use electricity as their process energy source and to optimise every step to reduce costs. Put out the call – innovation required!

To finish, let’s look at green iron. Note, I said green iron, not green steel. Steel is the desired end product, but producing it is a two-step process. The first step is to refine iron ore into iron. The second step is to combine the iron with other elements to make steel.

There is only one possible output of the first step – the element iron. However, there are many possible outputs from the second step, ranging from steel for building construction to stainless steel for surgical instruments. While traditionally these two steps take place in a single integrated plant, it is quite practical to separate them.

This represents an opportunity for Australia to add value to our iron ore by using zero-emissions processes to convert it into green iron before shipment. Today, nearly 8 per cent of global carbon dioxide emissions come from the first step in steelmaking. The most advanced approach to eliminating these emissions is to replace the blast furnace that uses metallurgical coal with a process called hydrogen direct reduction that uses electricity plus hydrogen instead of metallurgical coal.

Today, we ship the iron ore and the coal inexpensively to importing countries such as China, Japan, and South Korea. But shipping hydrogen is expensive and shipping renewable electricity is impractical. Hence, it makes tremendous sense to produce the green iron in Australia as a value-added product.

To date, hydrogen direct reduction has only been done anywhere in the world at pilot scale. It is essential to increase the efficiency and lower the costs by scaling up and optimising every step of the process. Put out the call – innovation required!

Hydrogen production underpins it all. The lead contender is to use renewable electricity to split water into its constituent ingredients – hydrogen and oxygen. The machines to do this are called electrolysers. The global electrolyser manufacturing industry is beginning to scale up but is still in its early stages. Efficiency must be improved, costs must be dramatically lowered, and the balance of plant must be integrated. Put out the call – more innovation required!

You will have noticed that all the decarbonised product export opportunities need lots of electricity. All up, the quantity of electricity that must be generated in Australia to operate vast numbers of electrolysers to make the hydrogen required will be in the hundreds of thousands of megawatts. That’s a lot of electricity and a lot of electrolysers.

The required growth in electrolyser manufacturing will be huge, off a small base. In 2022, the global deployment of electrolysers was only 130 megawatts for a cumulative installed capacity of 690 megawatts.

Can this be translated into an opportunity for electrolyser manufacturing in Australia? Absolutely. Unlike car manufacturing that failed, among other reasons, because of the relatively small domestic market, the Australian domestic market for electrolysers will be one of the biggest in the world. Unlike solar panels, electrolysers are extremely complex. Each one is a small factory, complicated to make and difficult to operate. Besides the stacks in which the water is split into hydrogen and electricity, there is electric power conditioning, water deionising, gas flow management, leak detection, air conditioning, gas dehydration, compression, and storage.

By manufacturing in Australia, we will reduce our dependence on international supply, avoid the cost and complications of international shipping and we will ensure that we have the skills and product knowledge required for deployment, operation, and maintenance. Tertiary training institutes and the manufacturing companies themselves will train the production workforce and there will be a spillover that will provide the field deployment and maintenance workforce.

Another reason to be confident that there is opportunity for electrolyser manufacturing in Australia is that because product development and manufacturing scale up are not yet mature, business innovation, geographic closeness to customers and manufacturing expertise will give newcomers a seat at the table. With the right policies in place, electrolyser manufacturing in Australia could be a boom industry, supporting our decarbonised-products export sector.

Australian built electrolysers will be deployed not far from where we mine iron ore to produce green iron. They will be deployed not far from sources of biomass so that we can produce hydrogen treated modern biofuels. They will be deployed close to ports and cheap renewable electricity so that we can economically produce green fertilisers, green marine fuel, and green jet fuel.

The challenge we face in Australia is to invest early and wisely. None of these decarbonised products are cheap or easy to establish, and there are other countries positioned as well as we are in at least some respects.

To pull it all together, to be a successful electrostate exporting embodied-hydrogen decarbonised products, we need a skilled workforce, targeted investments, government support to get us over the startup hump, gumption, good science, good engineering, and good project management.

Eventually these decarbonised products will be price competitive with conventional products, but like solar panels twenty years ago, they are much too expensive today. What would be the ideal policy response to accelerate the scale up and the cost reductions?

We cannot compete at the scale of the Inflation Reduction Act adopted last year in America. On the other hand, we cannot simply leave it to industry to sort out, given the enormous development costs and the substantial support that industries are getting from their governments in China, Japan, Europe, America, India, and elsewhere.

The transition to clean energy using renewable electricity and green hydrogen is underway and full of opportunity. The best approach for our federal and state governments is to pick a portfolio of opportunities in which to concentrate their financial and policy support.

Scale should be an essential criterion. On that basis, producing green iron in Australia is an obvious candidate, and similarly ensuring that we have the skills and industry to support hydrogen production is another obvious candidate.

A whole-of-sector regulatory opportunity for the Australian government is to ensure market transparency. Other than contaminants, green iron is indistinguishable from iron processed in a blast furnace using metallurgical coal. Green hydrogen is indistinguishable from hydrogen made from fossil fuels. Likewise, the other decarbonised products will be functionally indistinguishable replacements for the high-emission incumbents.

A vibrant international market in decarbonised commodities will require that buyers know the emissions intensity of the manufacturing process. Voluntary industry programs are unreliable, so it is pleasing to see that the Australian government has funded the Clean Energy Regulator to develop a certification scheme known as the Guarantee of Origin. Importantly, the government is already working with other national governments to ensure international recognition of the Guarantee of Origin scheme.

Government policies should not only support the exporters, but also the Australian innovators who develop and fine tune the enabling technologies. This will require that existing research and innovation programs in clean technologies, such as by cooperative research centres, the CSIRO, ARENA, and universities, are maintained and expanded. The Clean Energy Finance Corporation is operating effectively and being expanded.

For the ultimate in investment funding beyond government, our sovereign wealth fund and our superannuation funds are an enormous potential source. However, balancing their fiduciary duties to members and their willingness to take a chance for their long-term returns and the broader good is a difficult policy area. Difficult as it is, the opportunity is so large that it is worth returning to it even though it might feel like the discussion to date has gone round in circles.

In conclusion, Australia can be a winner as the world transitions to the Electric Age. But only if we focus on our areas of comparative advantage.

Dr Alan Finkel AC is a neuroscientist, engineer, entrepreneur, and philanthropist. He was Australia’s chief scientist from 2016 to 2020, during which time he led the development of the National Hydrogen Strategy and the panel that advised the Australian government on the Low Emissions Technology Roadmap, and was special adviser to the Australian government on Low Emissions Technologies in 2021 and 2022. Dr Finkel is chair of Stile Education and a corporate adviser on climate change technologies. His book, ‘Powering Up; Unleashing the clean energy supply chain’, was published in June.

Purchase a copy of the The Capability Papers here.

Do you know more? Contact James Riley via Email.